WORKING WITH DG ECHO AS AN NGO PARTNER | 2021 - 2027

13. FINANCIAL OVERVIEW OF THE ACTION

The purpose of this chapter is to present the financial elements of the Action. These data will allow DG ECHO to assess whether costs are necessary, reasonable and coherent with the results to be achieved. In case of partial funding, the feasibility of the Action will be assessed based on information about the sources of the financing of the Action.

2. Project Data Overview By Country

3. Humanitarian Organisations In The Area

4. Needs Assessment And Risk Analysis

12. Visibility, Communication And Information Activities

13. Financial Overview Of The Action

14. Requests For Alternative Arrangements

15. Administrative Information

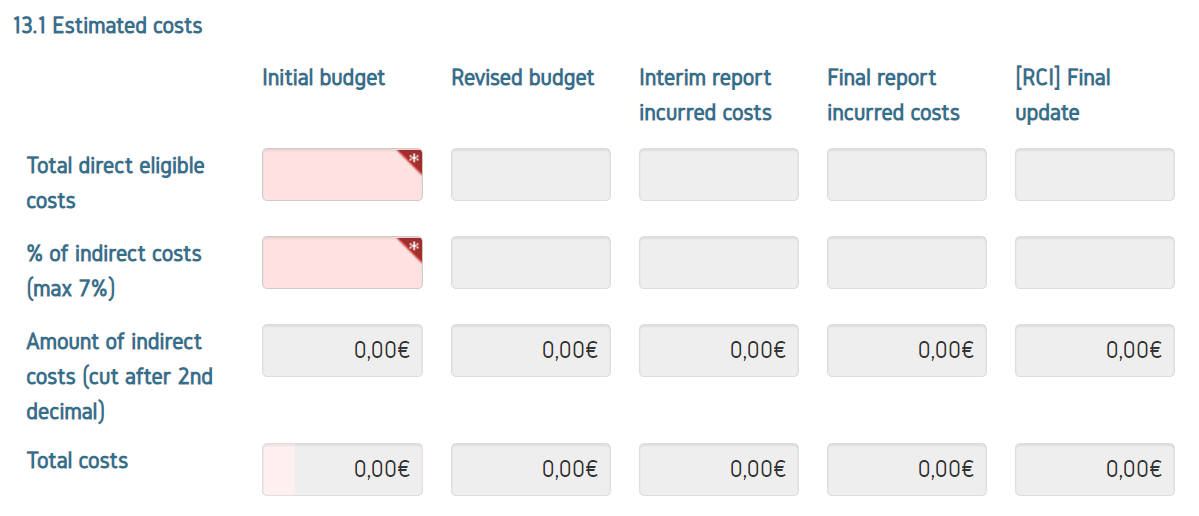

13.1 ESTIMATED COSTS

In this table the partner needs to provide the estimated total direct eligible costs and the percentage of indirect costs, while the rest will be automatically calculated.

All the financial amounts encoded in this section of the Single Form should be retrieved from the budget presented in the annex mentioned further down in the guidelines.

The indirect costs cannot be higher than 7% of the direct eligible costs.

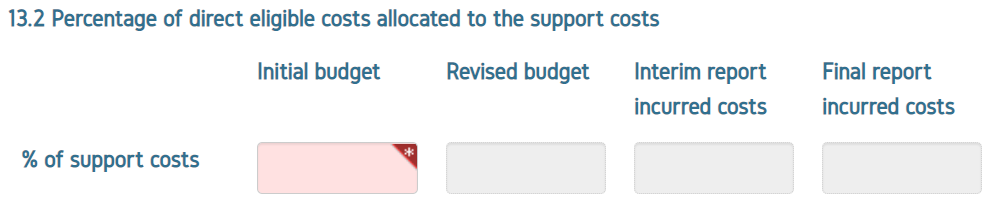

13.2 PERCENTAGE OF DIRECT ELIGIBLE COSTS ALLOCATED TO THE SUPPORT COSTS

In this section the Partner provides the % value of direct eligible costs allocated to support costs for this action.

The % provided in this section should be in line with the figures provided in the budget for each stage of the action. (RQ/MR/IR/FR).

The following definitions can help you to easier understand/distinguish the differences between various cost categories:

- direct costs: directly incurred to fund the activities described in the SF as necessary to the achievement of the results.

- direct support costs: costs under this title are also considered direct costs. They include field office costs, in particular:

- staff costs not delivering directly goods and services to the beneficiaries;

- running costs;

- local transportation to carry all necessary goods and material for the operation;

- distribution, storage and daily labour;

- security;

- feasibility, needs assessment and other studies;

- quality and quantity controls;

- external evaluation;

- insurance costs;

- visibility and communication programmes, etc.

- indirect costs: unless otherwise specified in the agreement, eligible indirect costs are declared on the basis of a flat rate of max 7% of the total eligible direct costs.

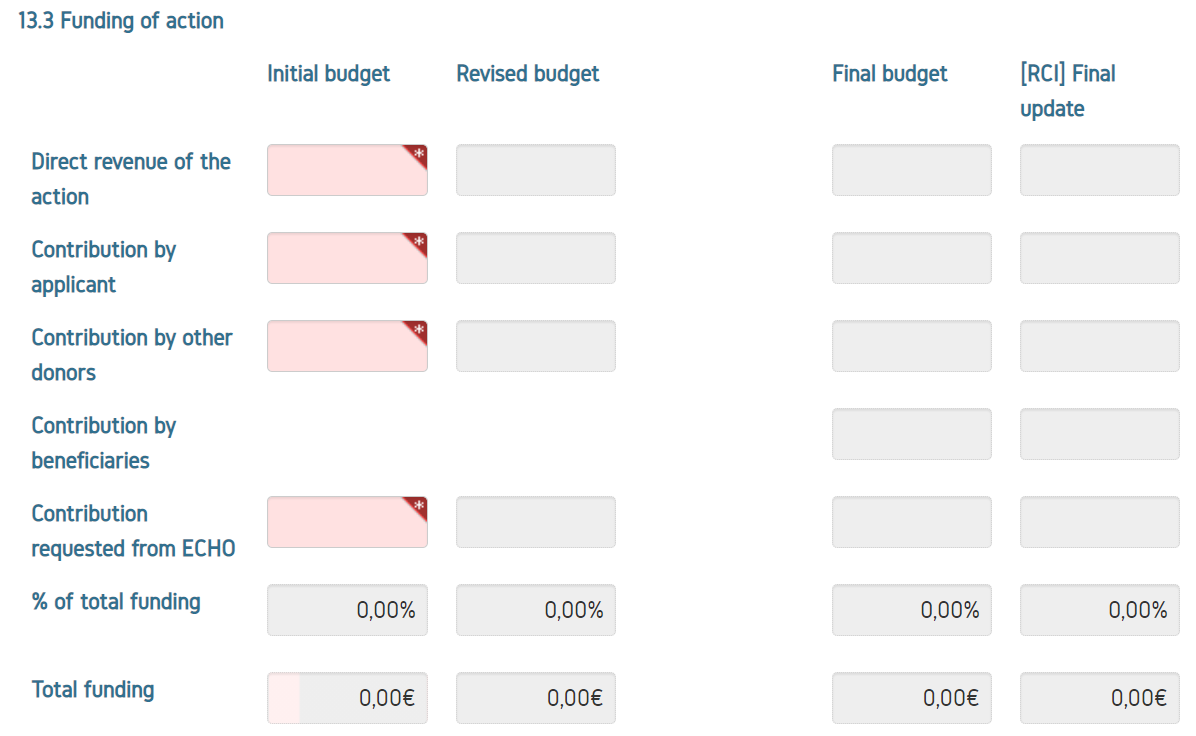

13.3 FUNDING OF THE ACTION

This section provides a picture of the various sources of financing. The table will be updated at interim and final stage.

- Direct revenue of the Action: this source of funding is quite exceptional and occurs when the Action itself creates income. In such cases, the final amount has to be mentioned here. At the proposal level, the partner can introduce an estimated amount if known.

- Contribution by applicant: if the partner (and co-partners if any) makes a contribution to the costs of the Action, it will mention here the foreseen amount.

- Contribution by other donors: it gives an indication of the approved and/or expected funding by other donors. At the final report stage, this information is based on real contributions.

- Contribution by final beneficiaries: these types of contribution are usually linked to cost recovery schemes. These amounts are considered as revenue of the Action.

- Contribution requested from DG ECHO: the expected funding from DG ECHO.

- % of total funding: it is automatically calculated by the system. In case the percentage is equal to 100%, the partner will have to provide a justification in section 13.4.

- Total funding: it is automatically calculated by the system and should be equal to the total costs of the Action mentioned under section 13.1.

13.4 EXPLANATION ABOUT THE 100% FUNDING:

This section has to be filled when contribution requested from DG ECHO equal 100% of the Action total funding as the exception to the principle of co-financing has to be duly and clearly justified.

The list of forgotten crisis is published on the ECHO website

13.5 YOU ARE EXPECTED TO UPLOAD IN APPEL THE ANNEX WITH DETAILED BUDGET

The budget is an annex to be filled in. For NGO partners, it is a requirement under the MGA, to increase comparability among actions and to better clarify the operational / support costs ratio. For further information on the compilation of this annex, please check the dedicated guidance in the budget template.

13.6 CONTRIBUTION IN KIND

When relevant, the partner has to provide here information on major in-kind contributions.

This allows crosschecking when in-kind contribution comes from other donors and whether the objective/results can be achieved when no expenses are foreseen for goods.

In-kind contribution (such as goods, equipment received for free) cannot be considered as contributions by the applicant in case of co-financing.

They can be described here to explain how they contribute to the success of the action, but they cannot be included in the total amount of the result nor in the financial statement.

13.7 FINANCIAL CONTRIBUTIONS BY OTHER DONORS:

The partner will briefly explain, when applicable, what will be the fall-back position in case of rejection of the funding request submitted to other donors.

In particular, additional explanations will be provided on whether this could lead to requesting more funding to DG ECHO or to reducing the volume of activities.

13.8 VAT EXEMPTION GRANTED

The default option is set on "yes". If the partner (or one of its IPs) already knows that the VAT exemption request has been rejected, the option "no" has to be selected.

In this case, the costs provided in the budget will have to include VAT. If the partner has selected the option “no” or "do not know yet", additional explanations need to be provided in section 13.8.1 on what actions have been or will be taken with the national authorities in order to obtain the VAT exemption.

It is the responsibility of the partner to report on the VAT status of all its Implementing Partners.

13.8.1 DETAILS ON VAT EXEMPTION (MANDATORY IF THE ANSWER IS "NO" OR "DO NOT KNOW YET")

If any VAT costs are declared by partner at the stage of final payment, the exact amount of total VAT claimed has to be provided. This includes the amounts charged through Implementing Partners.

Additionally partner should provide the date of the request made to the local tax authority and the date of rejection, if any.

If partner has not received any reply from the competent authority in the country of implementation, this has to been stated as well.

13.10 DO YOU INTEND TO INVOLVE AND CHARGE HQ STAFF COSTS TO PROJECT?

The default option is "No", as such costs are considered as eligible direct costs only in very specific cases.

If option selected is "Yes", explanations need to be provided in section 13.10.